This paper analyzes the relationship between tax avoidance and corporate social responsibility by companies listed on the Vietnam Stock Exchange. Since the interests of stakeholders and society are closely connected to corporate success, an increasing number of companies are incorporating social responsibility into their development plans. Conduct statistical description, correlation analysis and GMM regression analysis on a set of data comprising 210 companies that were listed between 2014 and 2022 on the stock markets in Hanoi and Ho Chi Minh City. Studies show that companies with a strong social responsibility program typically have lower rates of tax avoidance. This document supports businesses in developing strategies to achieve greater efficiency in the long-term development of the business while also providing advantages to relevant parties, such as tax authorities in establishing policies or investors in considering investment for a business.

Keywords: Corporate Social Responsibility; Cash Effective Tax Rate; Tax avoidance

Trách nhiệm xã hội của doanh nghiệp và thuế suất hiệu dụng tiền mặt: Bằng chứng từ các công ty niêm yết tại Việt Nam

Bài viết phân tích mối quan hệ giữa hành vi tránh thuế và trách nhiệm xã hội của doanh nghiệp tại các công ty niêm yết trên thị trường chứng khoán Việt Nam. Vì lợi ích của các bên liên quan và xã hội gắn liền với sự thành công của doanh nghiệp, ngày càng nhiều công ty đưa trách nhiệm xã hội của doanh nghiệp vào kế hoạch phát triển. Nghiên cứu thực hiện mô tả thống kê, phân tích tương quan và hồi quy GMM trên tập dữ liệu gồm 210 công ty niêm yết giai đoạn 2014-2022 trên thị trường chứng khoán Hà Nội và Thành phố Hồ Chí Minh. Kết quả cho thấy các công ty có chương trình trách nhiệm xã hội của doanh nghiệp mạnh thường có tỷ lệ tránh thuế thấp hơn. Kết quả nghiên cứu hỗ trợ các doanh nghiệp xây dựng chiến lược phát triển đạt hiệu quả cao hơn trong phát triển dài hạn, và đồng thời mang lại lợi ích cho các bên liên quan, chẳng hạn như cơ quan thuế trong việc thiết lập chính sách hoặc nhà đầu tư khi xem xét đầu tư vào doanh nghiệp.

Từ khóa: Trách nhiệm xã hội của doanh nghiệp; Thuế suất hiệu dụng tiền mặt; Tránh thuế.

JEL classification: M14, H25, G32, C23

https://doi.org/10.65771/ati-jas.04202609

1. Introduction

Corporate Social responsibility (CSR) has become more and more important to the operations of corporations in recent years. The World Business Council for Sustainable Development (2000) defined social responsibility as "Business's ongoing commitment to behave ethically and contribute to economic development while improving the quality of life of the workforce and their families as well as of the local community and society at large". By helping to balance and combine socioeconomic requirements and meet the expectations of investors, customers, and stakeholders, implementing social responsibility is an action that solves difficulties for company stakeholders, workers as well as communities. Businesses nowadays are successful not just because of their output and financial performance, but also because of the positive social impacts that they commit to and carry out. The most sustainable values are those that have a positive impact on individuals and the community, as the prosperity of businesses is closely linked to the well-being of society. As a result, Vietnamese businesses take social responsibility very seriously and integrate it into all aspects of their operations after realizing how important it is for business strategy.

While taxes are considered as a significant source of income for the state budget, they are also seen as an expenditure by businesses because they are an amount of money that need to be paid to the state. This allows the state to invest in vital areas and support community interests. In order to minimize the amount of tax paid and save as much operating cash as possible for their activities, businesses will also participate in tax avoidance (Yu et al., 2024). However, Wahab et al. (2022) pointed out that paying taxes is a measure that helps to guarantee social prosperity and Pasko et al. (2023) agree that a business's tax strategy is regarded as a component of its corporate social responsibility. Consequently, tax avoidance is still viewed as immoral activity even though it isn't illegal because it impacts everyone's interests in some way (Wahab et al., 2022).

Kovermann and Velte (2021) state that although there has been increasing attention to the connection between corporate social responsibility (CSR) and tax evasion, there is still uncertainty in the relationship, both empirically and philosophically. For example, Rashid et al. (2024) studied the connection between tax avoidance and corporate social responsibility (CSR) using a sample size of thirty Bangladeshi listed banks and came to the conclusion that the chance of tax avoidance behavior decreased with increasing CSR index. Ortas and Gallego-Álvarez (2020) attribute the different results in the correlation between tax avoidance and corporate social responsibility to cultural variations among countries.

This study contributes significantly in a number of aspects. Firstly, the existing literature reveals a fragmented and inconclusive picture of the CSR–tax avoidance nexus across different national contexts. In China, Gulzar et al. (2018) found a positive relationship, suggesting that CSR engagement can accompany greater tax avoidance, possibly as a reputational shield. In contrast, Yoon et al. (2021) reported a negative relationship in Korea, where ESG performance is associated with stronger tax compliance. Salhi et al. (2020) further demonstrated that the mediating role of CSR differs systematically between the UK (common law) and France (civil law): CSR fully mediates the governance–tax avoidance link in the UK but only partially in France. Taken together, these findings point to a clear research gap: results from developed and large emerging markets cannot be directly transposed to Vietnam’s institutional setting. Unlike the countries above, Vietnam operates under a civil-law tradition with a distinct corporate income tax regime, including preferential tax incentives and limited mandatory CSR disclosure requirements, which create unique incentive structures that may fundamentally shape how CSR commitments influence tax behaviour. Moreover, empirical evidence on this link in the Vietnamese market remains sparse. Our study therefore fills this gap by providing context-specific evidence from a frontier market where the interaction between CSR norms and tax regulation has yet to be thoroughly examined.

Second, the cross-country comparisons above underscore that legal frameworks and tax regulations are critical moderators of the CSR–tax avoidance relationship. Vietnam’s combination of civil-law governance, a socialist-oriented market economy and a tax system featuring industryspecific incentives and evolving transfer-pricing rules makes it a particularly instructive case for understanding how institutional context channels corporate tax behaviour. This study therefore presents a contextually grounded perspective that enriches the global evidence base.

There are six parts to the research paper. In the first part, the importance of corporate social responsibility (CSR) for firms is briefly discussed and some prior research on the association between CSR and tax evasion is outlined. The second section develops theories by presenting the theoretical foundations of the connection between tax avoidance and corporate social responsibility. The group outlines the data collection procedure and study methodology in part three. The results of the data processing and analysis process are shown in Part 4, and Part 5 is dedicated to ensuring that the results of Part 4 are sustained. The research group discusses the results, offers recommendations to relevant parties and provides the conclusions in part six.

2. Theoretical foundations, literature review and hypothesis development

2.1. Theoretical foundations and literature review

Three complementary theoretical perspectives underpin this study.

First, Stakeholder Theory (Freeman, 1984) holds that the existence of the firm requires the support of stakeholders; therefore, the activities of the firm also require their approval (Rokhlinasari, 2016). Stakeholders will provide tangible or intangible resources to ensure the survival and development of the business and businesses should therefore attend to stakeholder interests. The concept of stakeholders posits that enterprises participating in CSR as a means of social and ethical accountability share this duty with governments by paying the necessary taxes (Firmansyah et al., 2022). Because taxes improve society, they are intimately tied to CSR (Avi-Yonah, 2008). The government and the community’s interests as corporate parties can thus be aligned through the adoption of CSR initiatives.

Second, Agency Theory (Eisenhardt, 1989) highlights that agency problems arise when ownership and management are separated and the interests of the principal and agent conflict, resulting in suboptimal decisions. Voluntary CSR disclosure is one mechanism for reducing agency costs: managers release social responsibility information to demonstrate superior performance, reduce information asymmetry and allow external parties to monitor the firm more effectively (Fung et al., 2007). Disclosure requirements therefore have the potential to affect corporate behaviour in measurable ways, including changes in investment, resource allocation, and tax practices. Third, Legitimacy Theory (Deegan, 2011) frames the firm as a party to an implicit social contract with society. Enterprises that comply with societal norms and legal obligations maintain the trust of the community and secure their licence to operate. Effectively maintaining or restoring legitimacy requires demonstrating practical actions to inform stakeholders of the company’s payment of its “desired share of the tax” (Menicacci and Simoni, 2024). Taken together, these three theories predict that firms with strong CSR commitments will be less inclined to engage in tax avoidance, as doing so would undermine stakeholder trust, elevate agency costs through reputational risk and jeopardise the firm’s social legitimacy.

2.2. Hypothesis development

The impact of CSR on tax avoidance can be explained through two perspectives on business responsibility. Therefore, companies are more likely to view CSR as a strategic tool to manage or promote their business image. Due to less interest in CSR, they tend to apply the actual tax reporting method only in the form of tax avoidance or tax evasion. This can lead to the risk of being found under false tax reporting, which can damage a company’s reputation and cause public concern as well as media pressure (Hanlan and Slemrod, 2009). The reputational mechanism is central to understanding why CSR is associated with lower tax avoidance. A firm that actively invests in CSR signals to investors, customers, and regulators that it subscribes to broader social norms - including the obligation to contribute to public finances through tax compliance. Once a company has built its identity around ethical behaviour and stakeholder accountability, aggressive tax planning becomes directly inconsistent with that identity: the reputational cost of being exposed as a tax avoider, through media scrutiny, investor backlash, or regulatory investigation, outweighs the short-term financial benefit of tax savings. In this way, CSR commitment acts as a self-enforcing constraint on tax aggressiveness, because managers who are invested in protecting corporate reputation will voluntarily align the firm’s tax practices with its publicly stated social values (Godfrey, 2005; Menicacci and Simoni, 2024).

In contrast, according to Freeman (1984), companies emphasize not only the importance of shareholders but also of all stakeholders. According to the stakeholder theory, a company needs the support of its stakeholders in order to remain and as a result, the stakeholders must also approve of the company's operations (Rokhlinasari, 2016). CSR is an endeavor that enables a corporation to align with societal norms and values while demonstrating its commitment to the interests of all stakeholders. Tax, as a contribution to society, will be an integral part of CSR. Firms that prioritize social responsibility have lower rates of tax evasion. They are expected to pay their fair share of taxes (Lanis and Richardson, 2012).

According to Lanis and Richardson (2012), the tax authority should also be considered as a stakeholder of the business. They assume that the tax agency represents the government and represents the people. The purpose of the tax authority is to enhance the welfare of the community through tax collection and not just for their personal benefit. This can occasionally prompt them to prioritize social responsibility over profit maximization (Mackey et al., 2007). The effect of corporate social responsibility (CSR) on tax avoidance can be explained by the notion of corporate culture, which represents the infiltration of tax evasion into CSR activities, according to research results by Pasko et al. (2023). A business engages in CSR for the benefit of all parties involved, which already includes the government. Therefore, it is not possible to engage in active tax evasion. (Pasko et al., 2023). Ling and Liu (2023) assumes that companies interested in philanthropy will reduce tax avoidance. They found that companies that participate in corporate philanthropy (i.e. CSR) are less tax-deductible than their competitors. In support of this result, Kuo (2023) discovered that companies who did well in corporate social responsibility (CSR) had lower rates of tax evasion among their sample of 1.277 Taiwan-listed companies between 2015 and 2020.

Therefore, our study empirically tests the following research hypothesis:

H1: The social responsibility of the business has a negative impact on the tax avoidance behavior of the business.

3. Research Methodology

3.1. Data sources

We collect CSR and financial activity data from a database on the Vietnamese stock market (HOSE, HNX), one of the most widely used databases for accounting research related to Vietnam. Our initial sample includes all listed companies with financial and transactional data required for our research, listed on both hose from 2014 to 2022. Data are taken in the last 9 years to ensure the update and novelty of the study. However, the data used for the study does not include 2023 because it is to ensure the completeness and accuracy of the data. Finally, we obtained a valid sample of 210 businesses with selected businesses that provide qualifying metrics for results.

3.2. Definition of variables

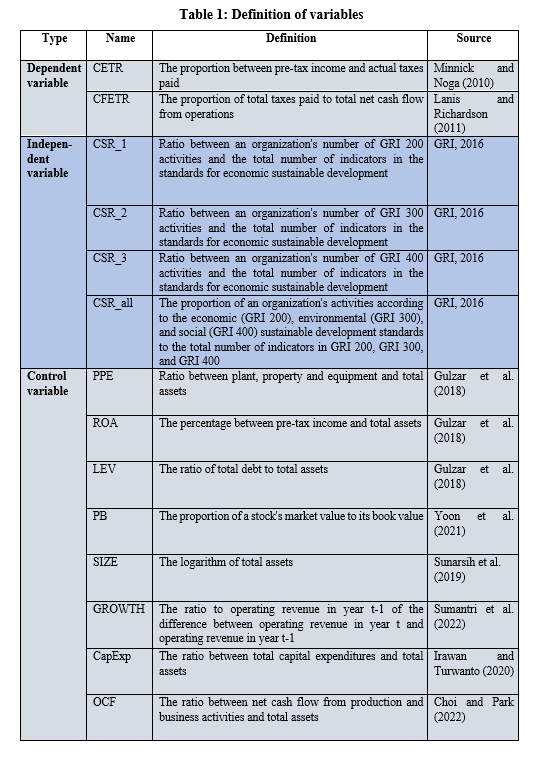

Based on the theory of stakeholders as the fundamental basis and earlier studies by Minnick and Noga (2010) and Lanis and Richardson (2011), we measure tax rates using the ETR variable as the dependent variable. Effective value of the business, where the ratio of actual tax paid to pre-tax income determines the CETR variable and the ratio of tax amount to total net cash flow from business activities determines the CFETR variable.

Measured according to GRI standards, the CSR variable is an independent variable that assesses corporate social responsibility in three areas: economic responsibility (CSR_1; 6 standards), environmental responsibility (CSR_2; 8 standards) and social responsibility (19 standards). In regards to this, the variables CRS_all and CSR_1, CSR_2 and CSR_3 are determined by dividing the total number of activities related to sustainable development standards in all three aspects that the enterprise implements by the total number of targets. Similarly, the variable CRS_all is determined by dividing the number of activities in each aspect that the business carried out by the number of indicators corresponding to that aspect.

The study group uses eight control variables, which are based on earlier research: (1) PPE, or the ratio of plant, property and equipment to total assets; (2) ROA, representing the ratio of pre-tax revenue to assets; (3) LEV, or financial leverage, is determined by dividing total debt by total assets; (4) PB, market value divided by book value of shares; (5) SIZE: the size of the firm, as determined by using the total assets' natural logarithm; (6) GROWTH: the ratio of operating revenue in year t-1 over operating revenue in year t-1, calculated as the difference between the two; (7) CapExp: the proportion of total assets to total capital expenditures (8) OCF: calculated as the ratio of total assets to net cash flow from operations and output. Table 1 displays the details of the above factors.

3.3. Model specification

The specific research model is as follows:

ETRi,t = α + β CSRi,t + γXi,t + ɛi,t

i = 1, 2, 3,…, 210 (i denoting the 210 listed businesses on the Vietnam Stock Exchange)

t = 1, 2, 3,…, 9 (t is the 9-year period from 2014 to 2022)

ETRi,t: Dependent variable, indicative of the company's effective tax rate at time t

CSRi,t: Independent variable, used to measure corporate social responsibility index i at time t

Xi,t: Control factors from earlier research are thought to have an effect on tax evasion

εi,t: The model's random error

4. Empirical Results

4.1. Descriptive statistics and correlation coefficients

Descriptive statistics

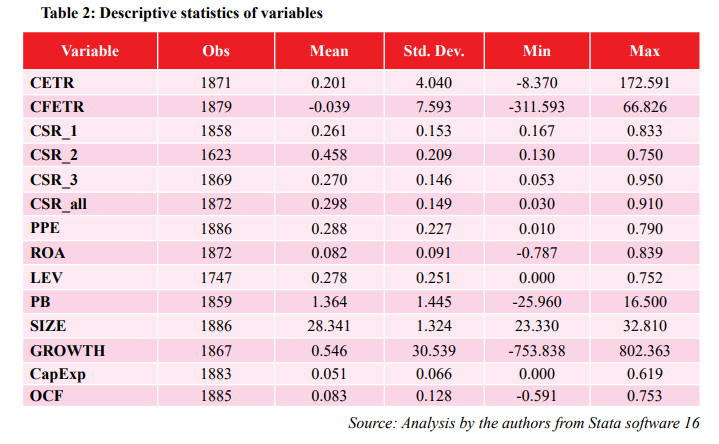

Table 2 shows the statistical results of dependent variables and independent variables for 210 enterprises listed on the Vietnamese stock market in the period from 2014 to 2022.

4.2. Regression results

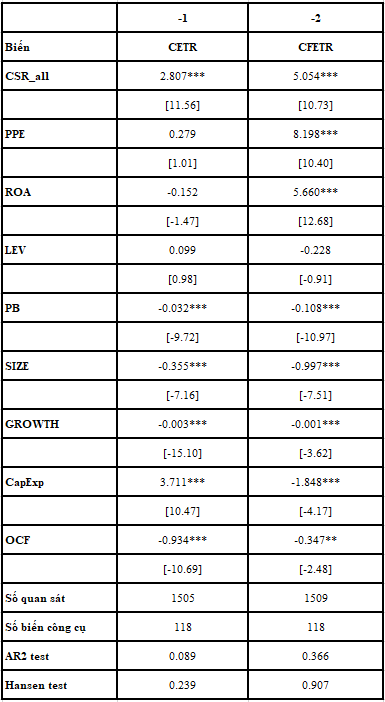

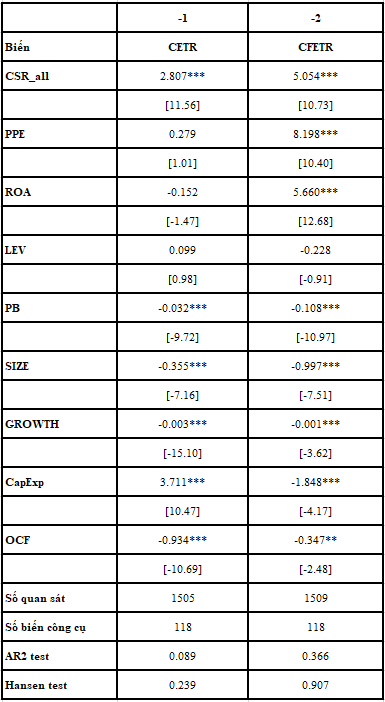

Table 3 shows the regression results related to the relationship between the social responsibilities of the enterprise and the tax avoidance behavior through representatives such as CETR and CFETR. The research sample is the data of the companies listed in the period 2014-2022 on the securities exchanges.

The regression results indicate that for model 1 when using the CETR variable as a dependent variable, for a positive correlation coefficient (2.807) and a high level of statistical significance with the CSR variable. Considering the model 2 with the CFETR dependent variable, the results are similar to the model 1 when social responsibility (CSR_all) and effective tax rate of the cash flow (CFETR) are positively correlated (= 5.054) and statistically significant. A consistent result between the two models and different ways of measuring dependent variables is that social responsibility has a positive impact on the effective tax rate of the enterprise. It is proven that the company's implementation of high social responsibility also increases the tax burden of the business. The authors determined that in the Vietnamese market, businesses use CSR as a way to reach out to stakeholders. Businesses use CSR to ensure their rights and bring more benefits to society so it is easy to understand that when the company is highly rated on CSR, their tax rate is high or tax avoidance is low. The company implements CSR to enhance its reputation, so the use of tax avoidance policies can lead to reputational damage in society. If there is a balance between minimizing the tax burden and the reputational impact of leaking information about tax avoidance, managers will be more willing to protect corporate reputation. Since then, a business with high Corporate Social Responsibility does not usually apply activities that reduce the number of taxes to be paid.

Table 3: GMM regression results

Source: Analysis by the authors from Stata software 16

Note: ***, **, * * are statistically significant at 1%, 5%, 10%, respectively. The numbers in parentheses represent the z-value

For control variables, there are negative relationships between PB, SIZE and GROWTH, OCF and CETR, CFETR, significant at the 1% level. This means that the larger the Share Value, Size and Growth of the business, the less likely they are to be tax heavy or the more likely they are to use tax avoidance methods. This result can be explained by the correspondence with the growth of the business or the fact that the business can balance its resources to make a tax plan in accordance with the financial decisions aimed at positively impacting the pre-workflow as well as leading to reduced tax rates. CapExp variable (Capital Expenses) has a positive impact on the amount of tax that must be submitted (CETR), significant at the 1% level. The company plans to invest capital to consider financial efficiency from the decision to invest in expanding or replacing fixed assets and this gives the business the opportunity to increase its production capacity and income, so that the business can also pay more. PPE and ROA have a positive relationship on CFETR and the result is significant at the 5% level. A business that has a high ROA value and invests a lot in multiple formatted fixed assets will often pay taxes more fully and honestly rather than looking for ways to reduce the amount of taxes that must be paid. But the financial promotion (LEV) results have no effect on the effective tax rate in both models.

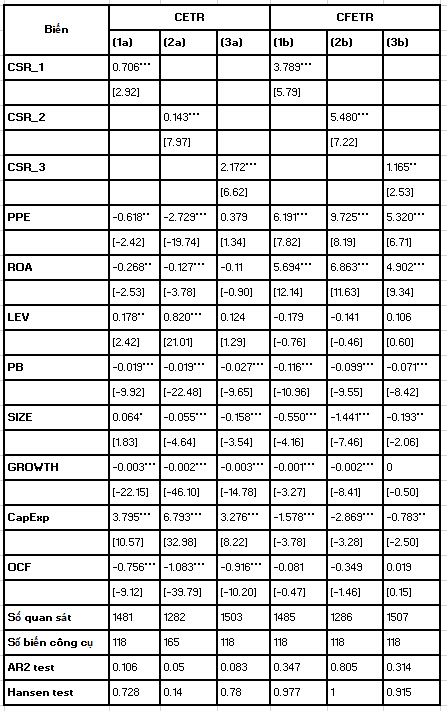

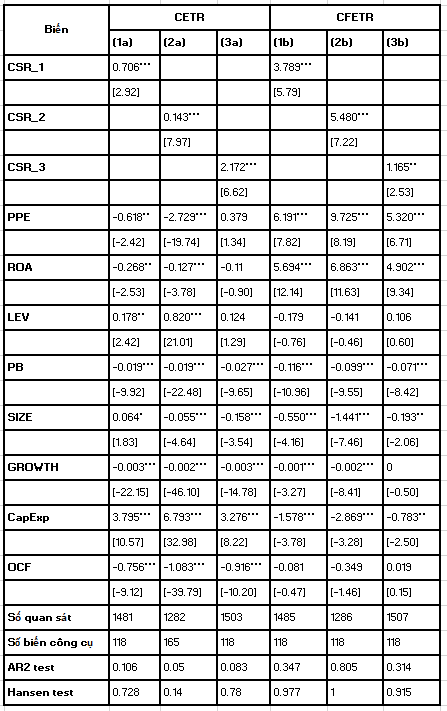

5. Robustness tests

To confirm the accuracy of the GMM regression results shown in Table 4, the team replaced the CSR_all independent variable into each variable representing each indicator of corporate social responsibility, respectively, economic (CSR_1), environmental (CSR_2) and social (CSR_3) indicators and re-estimated the proposed model.

Table 4: Regression results to ensure sustainability

Source: Analysis by the authors from Stata software 16

Note: ***, **, * * are statistically significant at 1%, 5%, 10%, respectively. The numbers in parentheses represent the z-value.

Table 4 shows that when regression with the variable CETR is a dependent variable and the variable CSR_1 is an independent variable (model 1a), the results show a positive correlation index and high statistical significance (CSR_1 = 0.706, t = 2.92); the results when CSR_2 and CSR_3 are independent variables in model 2a and model 3a are similar (CSR_2 = 0.143, t = 7.97; CSR_3 = 2.172, t = 6.62). From this, it can be seen that social responsibility in economic, environmental, and social indicators all have a positive impact on the effective tax rate of the enterprise and this matches the outcomes shown in Table 3. At a significance level of 1%, the PB (price-tobook ratio), SIZE, GROWTH and OCF (net cash flow from operating activities) variables show a negative relationship with CETR, and the CapExp variable has a positive impact on CETR, which is similar to the results presented by the team. From this, it can be seen that social responsibility in economic, environmental and social indicators all have a positive impact on the effective tax rate of the enterprise, which is consistent with the results that the group has regressed with the independent variable CSR_all. The control variables PPE and ROA were positively correlated with CFETR and the control variables PB, SIZE, GROWTH and CapExp were negatively correlated with CFETR.

6. Conclusion and policy implications

This article's goal is to investigate the connection between tax evasion and disclosure of corporate social responsibility (CSR). The authors' hypothesis is that there is a negative correlation between tax avoidance and CSR initiatives. The authors do quantitative research using the GMM regression approach on a sample of 210 companies listed on the Vietnam Stock Exchange between 2014 and 2022. Based on the findings, the team concluded that CSR positively affects effective corporate income tax; in other words, businesses that engage in social responsibility initiatives are less likely to engage in tax evasion. The results are consistent with the hypothesis set by the team.

Regarding the inconsistent results on the correlation between tax avoidance and corporate social responsibility (CSR), Ortas and GallegoÁlvarez (2020) clarified that cultural disparities exist among nations. Countries with long-term goal orientation - always focusing on perseverance and consistency in work, tolerance and opportunities for dialogue with stakeholders - will often have a negative relationship between CSR and tax avoidance. CSR will have a less negative impact on tax avoidance in countries with high differences in the power of individuals and members of society who are insecure in the face of uncertain and ambiguous situations, reducing the dialogue between the parties.

Based on the aforementioned study findings, the authors have recommended the following to investors, companies and tax authorities in order for them to have the proper policies for themselves:

For investors: Investors should consider an enterprise's tax compliance behavior in addition to its basic financial indicators when considering an investment. This is because companies that comply with tax laws typically have good business practices and high return on assets (ROA), which demonstrate the efficient use of capital by the company. Furthermore, these companies have greater credibility in the stock market.

For listed companies: Although tax avoidance acts bring immediate benefits to the company (reducing tax costs for businesses), in the long run it will affect the reputation as well as corporate public position in both tax authorities and the whole society. In contrast, actively improving environmental protection behavior of enterprises, full and transparent information disclosure as well as good implementation of tax obligations will help the company build a long-term reputation for investors, society and the government. Currently, not only Vietnam but other countries are very interested in CSR and tax avoidance, so if businesses want to build a good image to improve business results or attract more investors, they should actively disclose their tax information and social responsibility in the most complete and transparent way.

For the Ministry of Finance and regulatory authorities: The findings of this study carry specific implications for policy design at the national level. The evidence that higher CSR engagement is associated with a lower degree of tax avoidance suggests that promoting voluntary and mandatory sustainability disclosure can serve as an effective indirect mechanism for enhancing tax transparency. The Ministry of Finance should consider introducing a regulatory framework that formally links the publication of ESG or CSR reports - particularly those prepared in accordance with internationally recognised standards such as GRI or ISSB - to measurable tax transparency obligations. Concretely, this could take the form of: (i) granting preferential corporate income tax treatment or expedited tax refund procedures to companies that publish audited sustainability reports meeting prescribed disclosure standards; (ii) requiring companies that disclose ESG/CSR data to include a dedicated tax transparency section that reports their effective tax rate, the nature of tax incentives utilised and any material transferpricing arrangements; and (iii) incorporating CSR disclosure quality as a positive indicator within the annual tax compliance risk-rating system applied by the General Department of Taxation. Such measures would create a virtuous cycle in which enhanced social accountability reinforces responsible tax behaviour, thereby broadening the tax base while rewarding companies that genuinely commit to sustainable and ethical business practices.

In general, the research contributes to supporting the CSR perspective as a stakeholder approach. Businesses can also utilize CSR as a means of using their tax obligations to give back to the community and society. It is evident that CSR helps to uphold a company’s reputation and brand in the marketplace, which draws in more devoted partners, investors, and clients and raises the company’s worth. Moreover, the advantages of putting CSR into practice, such as tax compliance, outweigh the advantages of tax evasion.

References

1. Choi, J., & Park, H. (2022). Tax avoidance, tax risk, and corporate governance: evidence from Korea. Sustainability, 14(1), 469. https://doi.org/10.3390/su14010469;

2. Freeman, R. E. (1984). Strategic management: A stockholder approach. Pitman;

3. Fung, A., M. Graham, and D. Weil. 2007. Full Disclosure: The Perils and Promise of Transparency: Cambridge University Press;

4. Godfrey, P. C. (2005). The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Academy of management review, 30(4), 777-798. https://doi. org/10.5465/amr.2005.18378878;

5. GRI Standards (2016). Consolidated Set of GRI Sustainability Reporting Standards. Global Sustainability Standards Board;

6. Gulzar, M. A., Cherian, J., Sial, M. S., Badulescu, A., Thu, P. A., Badulescu, D., & Khuong, N. V. (2018). Does corporate social responsibility influence corporate tax avoidance of Chinese listed companies?. Sustainability, 10(12), 4549. https://doi.org/10.3390/su10124549;

7. Hanlon, M., & Slemrod, J. (2009). What does tax aggressiveness signal? Evidence from stock price reactions to news about tax shelter involvement. Journal of Public economics, 93(1-2), 126-141. https://doi.org/10.1016/j.jpubeco.2008.09.004;

8. Irawan, F., & Turwanto, T. (2020). The effect of tax avoidance on firm value with tax risk as a moderating variable. Test Engineering and Management, 83(March-April), 9696-9707;

9. Kovermann, J., & Velte, P. (2021). CSR and tax avoidance: A review of empirical research. Corporate Ownership and Control, 18(2), 20-39 https://doi.org/10.22495/cocv18i2art2;

10. Kuo, C. S. (2023). Corporate social responsibility and tax avoidance: Evidence from the 2018 tax reform in Taiwan. Review of Pacific Basin Financial Markets and Policies, 26(01), 2350007. https://doi.org/10.1142/S0219091523500078;

11. Lanis, R., and Richardson, G. 2011. The effect of board of director composition on corporate tax aggressiveness. Journal of Accounting and Public Policy 30(1): 50–70. https://doi.org/10.1016/j. jaccpubpol.2010.09.003;

12. Lanis, R., & Richardson, G. (2012). Corporate social responsibility and tax aggressiveness: An empirical analysis. Journal of Accounting and Public policy, 31(1), 86-108. https://doi. org/10.1016/j.jaccpubpol.2011.10.006;

13. Ling, Q., & Liu, L. (2023). Corporate giving and the case of tax avoidance. Advances in Accounting, 61, 100638. https://doi.org/10.1016/j.adiac.2023.100644;

14. Mackey, A., Mackey, T. B., & Barney, J. B. (2007). Corporate social responsibility and firm performance: Investor preferences and corporate strategies. Academy of management review, 32(3), 817-835. https://doi.org/10.5465/amr.2007.25275676;

15. Menicacci, L., & Simoni, L. (2024). Negative media coverage of ESG issues and corporate tax avoidance. Sustainability Accounting, Management and Policy Journal, 15(7), 1-33. https://doi. org/10.1108/SAMPJ-01-2023-0024;

16. Minnick, K., & Noga, T. (2010). Do corporate governance characteristics influence tax management?. Journal of corporate finance, 16(5), 703-718. https://doi.org/10.1016/j. jcorpfin.2010.08.005;

17. Ortas, E., & Gallego-Álvarez, I. (2020). Bridging the gap between corporate social responsibility performance and tax aggressiveness: The moderating role of national culture. Accounting, Auditing & Accountability Journal, 33(4), 825-855. https://doi.org/10.1108/AAAJ-03-2017-2896;

18. Pasko, O., Zhang, L., Oriekhova, A., Hordiyenko, M., & Tkal, Y. (2023 ). Corporate social responsibility and corporate tax aggressiveness: Evidence of mandatory vs. voluntary regulatory regimes impact. Problems and Perspectives in Management, 21(2), 682-700 http://dx.doi. org/10.21511/ppm.21(2).2023.61;

19. Rashid, M. H. U., Begum, F., Hossain, S. Z., & Said, J. (2024). Does CSR affect tax avoidance? Moderating role of political connections in Bangladesh banking sector. Social Responsibility Journal, 20(4), 719-739. https://doi.org/10.1108/SRJ-09-2022-0364;

20. Rokhlinasari, S. (2016). Teori-teori dalam pengungkapan informasi corporate social responbility perbankan. Al-Amwal: Jurnal Ekonomi dan Perbankan Syari'ah, 7(1);

21. Salhi, B., Riguen, R., Kachouri, M., & Jarboui, A. (2020). The mediating role of corporate social responsibility on the relationship between governance and tax avoidance: UK common law versus French civil law. Social Responsibility Journal, 16(8), 1149-1168. https://doi.org/10.1108/SRJ-04-2019-0125;

22. Stiglingh, M., Smit, A. R., & Smit, A. (2022). The relationship between tax transparency and tax avoidance. South African Journal of Accounting Research, 36(1), 1-21. https://doi.org/10.1080/10 291954.2020.1738072;

23. Sumantri, F. A., Kusnawan, A., & Anggraeni, R. D. (2022). The Effect Of Capital Intensity, Sales Growth, Leverage On Tax Avoidance And Profitability As Moderators. Primanomics: Jurnal Ekonomi & Bisnis, 20(1), 36-53. https://doi.org/10.31253/pe.v20i1.861;

24. Sun H, Yang M, Li L, Liu C. Corporate Charitable Donations, Earnings Performance and Tax Avoidance. Sustainability. 2023 https://doi.org/10.3390/su15043116;

25. Sunarsih, S., Haryono, S., & Yahya, F. (2019). Pengaruh Profitabilitas, Leverage, Corporate Governance, dan Ukuran Perusahaan Terhadap Tax Avoidance (Studi Kasus Pada Perusahaan Yang Tercatat Di Jakarta Islamic Index;

26. Wahab, N. A., Rahin, N. M., & Mustapha, M. Z. (2022). CSR decoupling and tax avoidance: a conceptual framework. Australasian Accounting, Business and Finance Journal, 16(3), 131-146. https://doi.org/10.14453/aabfj.v16i3.09;

27. Yoon, B., Lee, J. H., & Cho, J. H. (2021). The effect of ESG performance on tax avoidanceEvidence from Korea. Sustainability, 13(12), 6729. https://doi.org/10.3390/su13126729;

28. Yu, X., Chen, M., & Ye, Y. (2024). Multiple Large Shareholders, Investment Efficiency and Corporate Tax Avoidance: Evidence from China. Prague Economic Papers, 33(1), 103-136. https:// doi.org/10.18267/j.pep.85.

Ngày nhận bài: 05/02/2026

Ngày biên tập: 13/02/2026

Ngày duyệt đăng: 30/03/2026

Tác giả:

Nguyen Vinh Khuong

Nguyen Ngoc Hong Phuc

Nguyen Huynh Nhu Phuong

Nguyen Vo Nhat Kieu

Hoang Thi Trinh

Nguyen Thi Diem Thy

Faculty of Accounting and Auditing, University of Economics and Law, Vietnam National University, Ho Chi Minh City, Vietnam

Email: khuongnv@uel.edu.vn